6 Realistic Cases for Implementing Agentic AI in Retail Banks

Development

Reading time

6

mins

As in every other industry, finding a place for agentic AI has become one of the most discussed topics in banking. BCG estimates that AI agents could raise banks' profitability by 30% and reduce costs by 30 to 40% by 2030, numbers aimed straight at the two things every bank works to improve.

So naturally, banks started to explore what the new technology could take off their hands, seeing in it a way to clear out the routine work and buy back valuable time.

As is typical when navigating territory as new as AI, many of those initial deployments are still catching up to the ambitious expectations set for them.

Part of the reason is that under the pressure to modernise, keeping pace with market expectations started to matter as much as what the projects delivered.

That is why this article takes a more grounded look at where the value of agentic AI lies for banks, and where introducing agents makes sense once you factor in the deeply embedded infrastructure banks rely on to function.

Understanding Agentic AI in retail banking

If terms like AI automation, copilots and chatbots already sound like the same thing to you, agentic AI probably landed on that pile too.

So let's clear up what it means before we go anywhere near banking systems.

Agentic AI refers to autonomous systems that plan, execute and adapt across workflows with minimal human intervention. A system like this receives a goal, works out the actions needed to reach it and carries them out across multiple tools, data sources and channels.

In simple terms, you tell it what needs to be done and it works out the steps to complete the entire task on its own.

Say the job is getting a loan application ready for a decision.

Now, once that instruction reaches an agentic system, the first thing it would do is pull the applicant's statements and run the affordability numbers against them.

If it hits a gap in the file, let's say a payslip the applicant never attached, it goes back and requests the document on its own.

Scripted software would have stalled right there and waited for someone to notice.

And at the end of all this, the person gets back either a complete application or a note saying the income couldn't be verified and the case needs a human look.

What would make a system in banking truly agentic?

First, it should work toward an objective and break that objective into the tasks required to reach it.

If a bank gave it the objective of verifying a new business client, the agent itself would determine that this means pulling the company's registry record, then screening the owners against the watchlists, and then requesting whatever document the file still lacks.Second, its planning must be dynamic. A system that follows a script can only handle the cases the script anticipated, so an unusual case stops it. An agent reads the input actually in front of it and determines the appropriate course of action there and then.

Third, it holds a real degree of autonomy over how the work gets done. If someone has already decided every step and every tool in advance, then the system is merely executing a plan a human made, and that is the ordinary automation banks have run for years. An agent makes the plan itself and chooses its own route through the tools it has been permitted to use.

If the Agentic system can act on its own, where does that leave people running the bank's operations?

They must remain in the loop, at every important step that carries security weight for the bank.

There may come a time when agents coordinate with other agents and carry entire operations between themselves, but an agent in a bank works inside the systems that hold accounts, process payments and keep the records regulators audit, and those systems took decades to build and connect.

Where agentic AI realistically fits in a retail bank

Banks handle enormous volumes of documentation every day, and language models have already found their place there, digesting loan files and reports and returning the short version that once took an analyst an afternoon.

Useful as that is, a summary only tells someone what the data says.

The person still analyzses what it means for the case in front of them and then carries the result into the next system, and most of the working hours in a bank's operations sit in that carrying.

The more realistic gain lies in connecting all three, the mass of data, the analysis of it and the execution of what the analysis calls for, inside one process instead of three hand-offs.

The cases below run through the parts of the bank where that connection matters most, and each one shows what an agent takes over and what stays with the person.

1. Agent-driven fraud detection and AML compliance

Every bank runs monitoring systems that raise an alert whenever a transaction looks off, and in traditional anti-money-laundering programmes up to 95% of those alerts turn out to be false positives.

AML officers still have to clear each one, and because the evidence sits scattered across separate systems, an analyst can spend four or more days preparing a single Suspicious Activity Report, the document banks file to the authorities.

The judgment itself takes minutes once the evidence sits in one place. Everything before it is collection, and collection is where much of the 35 to 40 billion dollars US banks spend on these operations every year goes.

What makes an agent realistic here, and BCG's report makes this point well, is that the detection itself already works.

The monitoring, the screening and the identity checks are validated systems the bank has trusted for years, and the missing piece has always been the layer that reads their combined outputs, which until now meant a person.

An agent would sit in that reading layer, inside the bank's existing risk and compliance framework, and bring the analyst a prepared case with its reasoning laid out next to each finding.

Only the final decision would remain outside the agent's hands, because a Suspicious Activity Report carries legal weight and the bank's reputation with it, so a compliance officer should review the case the agent prepared and stand behind the call to file it.

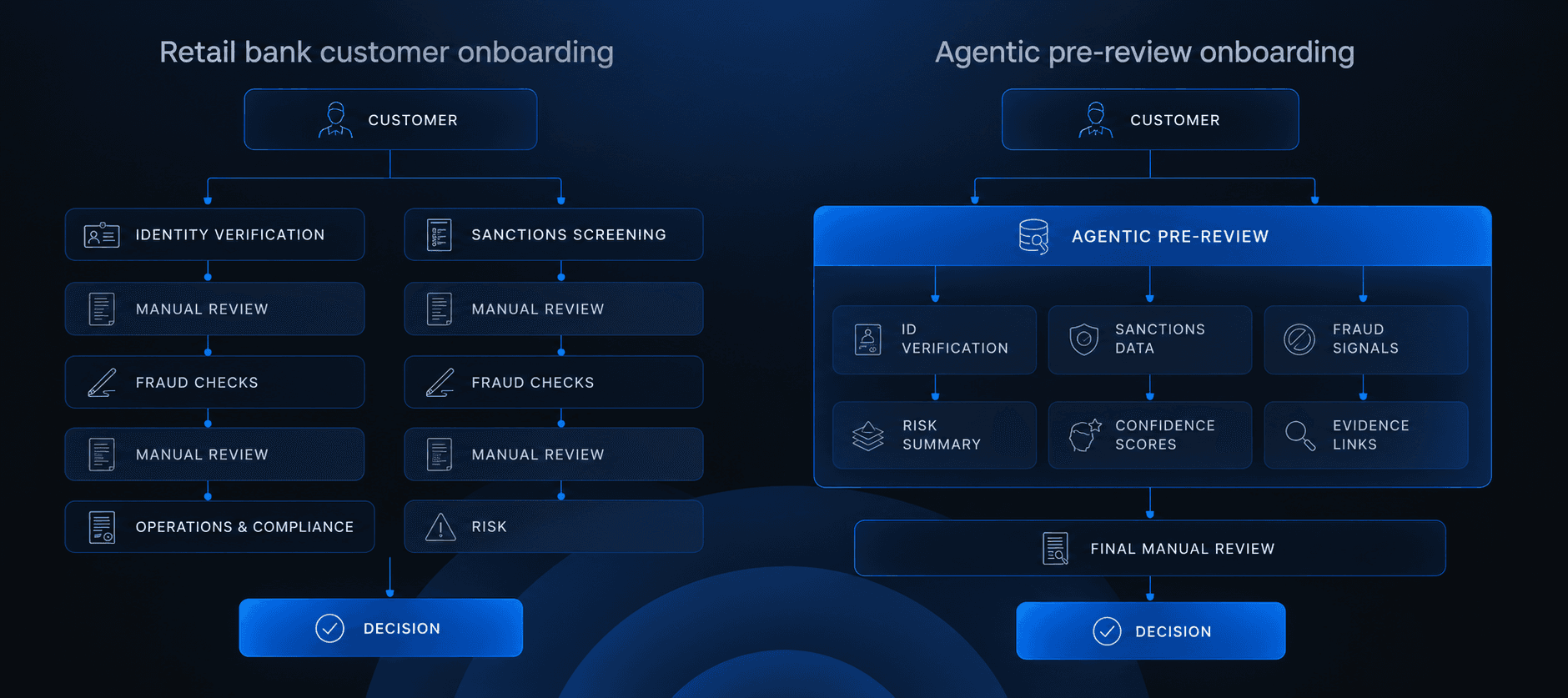

2. Streamlining customer verification and onboarding

If you've recently opened an account on any financial platform, you already know the onboarding can drag.

The reasons you waited for the approval comes down to the fact that identity, credit, and compliance checks all live in completely separate systems.

Right now, a human employee has to sit there, cross-reference the disconnected data by hand, and build your profile from scratch.

In fairness, the carefulness in the process makes sense, since the bank is handling sensitive personal data and answering for every customer it lets in.

Rather than making staff play detective across different screens, an agentic system would act as the connective tissue.

It could read the combined background checks, realise when a piece of the puzzle is missing (like a forgotten proof of address), and automatically chase the applicant for it.

It would only hand the file over when it could deliver a complete, structured profile with a clear rationale, ensuring everything stayed inside the bank's existing risk framework.

3. Accelerating credit underwriting and loan approvals

Anyone who has waited on a loan decision knows it takes days and often weeks, and 8 to 12% of applicants abandon their application before the response arrives.

At most banks, a credit analyst still puts each file together manually, reconciling the applicant's records across separate systems and summarizing them into a memo the credit officer can decide on.

An agentic system placed here could do that initial analysis of the applicant's profile for the analyst, reading what the bank's identity checks, credit bureau data and fraud signals returned and producing a structured risk summary with each figure traced back to its source, so the analyst would start from a prepared file and spend the saved hours on the cases that genuinely need working through.

The bank's own underwriting models would keep assessing credit risk and affordability the way they always have, since the agent's work would end at the summary it hands over, and the officer's decision would rest on it.

4. Resolving back-office exception handling automatically

A surprisingly large part of a bank's workforce never works with customers directly, since 50 to 60% of a bank's full-time staff work in operations, on the reconciliations, payment investigations and dispute cases running behind every product the bank offers.

Banks automated much of this work years ago, and the automation that came out of it only covered the standard cases, because a tool with predefined rules can't exactly react to the even smallest mistake like payment arriving with a mistyped reference number, which is why the case circled back to the operations staff.

An agentic system could resolve it instead, reading the records on both sides of the transaction, working out where the two disagree, correcting the reference if that sits within its authority and escalating the case if it doesn't, with every step logged for the team to trace afterwards.

Banks running early deployments of this kind report manual workloads reduced by 30 to 50%.

Running this in production would take more than the agent itself.

A bank would need a repeatable way of measuring the agent against the same exception cases its human teams resolve today, tracking the quality of its work as models and workflows change, and it would need a single control layer through which all of its AI applications pass, where access rules hold for every agent equally and every decision leaves a trace in one log, so that unusual behavior surfaces quickly and a misbehaving agent gets switched off before its errors spread through systems that all depend on each other.

5. Delivering end-to-end customer service resolution

Traditional banking chatbots are highly effective at answering routine questions and routing customers to the right departments, but they generally hit a wall when a request requires actual database changes.

An agentic system, by contrast, would bridge the gap between conversation and core system execution.

For example, if a customer flagged an unrecognised charge, the system wouldn't just explain how to file a claim; it would handle the underlying process.

It would query the transaction database, cross-reference the merchant history, and evaluate the claim against the bank's existing fraud policies.

If the request met the safety criteria, the agent could authorise a provisional credit and log the formal dispute automatically, resolving the entire issue within a single chat session.

McKinsey's partners report that AI-powered call centres and bots already handle the majority of customer interactions at leading institutions, and the depth of resolution is where the current work is concentrated.

There is also a strategic reason to care about this case beyond the cost of the contact centre.

McKinsey has mapped a scenario in which third-party AI agents become the customer's primary banking interface within three to five years, shopping for products and executing transactions on the customer's behalf while the bank recedes into a supplier behind someone else's interface.

6. Driving intelligent customer engagement and personalisation

Conversational AI already operates at a massive scale in retail banking. Bank of America’s assistant, Erica, is a prime example, having crossed 3 billion client interactions for nearly 50 million users.

However, user satisfaction has not matched this rapid adoption.

When Deloitte surveyed US banking customers, they found that while traditional bots handle routine queries well, they fail to inspire confidence when problems grow complex, often trapping customers in rigid menu structures.

An agentic system would resolve this by focusing on resolution rather than navigation.

In the case of an unrecognized card charge, the agent would investigate the transaction across the customer's accounts, open the dispute, and follow it through the bank's process right inside the conversation. When the dispute required a complex judgment call, the agent would seamlessly transfer the fully documented file to a human specialist.

The customer would only have to explain their situation once, and the bank would eliminate the typical queues between departments.

Implementing this would require a foundational control layer to manage access rights and log every decision.

This would ensure that the agent operates strictly within compliance boundaries while maintaining a complete audit trail for regulators.

Navigating implementation, risk, and governance

Bringing agents into a bank is a question of organisation before technology.

The experience so far shows efforts scattered across many pilots that never scale, which is why the sensible path runs through one cross-functional team with the authority to choose a handful of projects and see them into production under clear ownership.

Governance would need to grow alongside that work, since an AI-assisted workflow has to stay auditable and answerable to the bank's existing control functions the same way any human-run process already is.

And an agent can't be validated once and left alone, because the models underneath it keep changing along with how people use them, so the testing has to continue for as long as the agent runs, less a launch requirement than a permanent operating discipline.

Setting up the right team and governance structure is usually the hardest part of this journey. If you are looking for a starting point, check out our guide on how to scale AI in banking for a look at how to structure your strategy from day one.