Escaping AI Pilot Purgatory: How Can Banks Scale AI to Production (Without Replacing Legacy Cores)

Jun 29, 2026

Development

Reading time

8

mins

When one of the world's largest banks deployed AI, believing it would resolve customer inquiries faster and better, leadership was confident enough to immediately cut dozens of call center roles.

Within just a few weeks, they were forced to call the same employees to offer them their jobs back.

The AI chatbot wasn’t remotely equipped to handle complex, non-standard inquiries, which only compounded the pressure on the remaining support staff.

While the bank faced a public relations nightmare, the situation didn’t force them to give up on the technology. Instead, they took a step back and rebuilt its strategy from the ground up.

By fixing the structural flaws in their operating model rather than blaming the AI, they eventually turned an expensive operational failure into a system that actually handles high-volume requests without breaking down.

Banks across the industry are currently trying to find a way to replicate that turnaround investing heavily, yet struggling to see an impact that can be operationalised at scale.

Sure, when you look at recent MIT’s project NANDA research showing that 95% of corporate pilots fail to produce a measurable financial return at the enterprise level, or IDC data proving that only about 4 out of every 33 AI proofs of concept ever make it into production, you might think that enterprise AI is a fundamentally broken promise.

But that data only tells one small part of the story.

Deploying AI and maximising its benefits requires far more than just “plugging” chatbot or an autonomous agent.

The real obstacles remain structural: legacy architectures, disconnected departments, and fragmented data silos.

Yet, despite what the macro statistics suggest, we are seeing a period of incredibly rapid learning and iteration.

Many banking pilots are achieving phenomenal technical results and delivering real value at the team or individual level, even if they haven’t yet been scaled across the entire organisation.

Most bank executives will tell you that these high failure rates aren't actually concerning.

AI allows them to experiment at a fraction of the cost they spent before as building and testing a concept used to require months of preparation and substantial capital investments.

The question isn't whether AI works, but how to clear the operational path for it.

Drawing directly from our recent experience building automated document and data pipelines for a retail bank, we’ve written this guide for banking executives to outline the exact framework required to move past localised testing and scale AI into production, starting with targeted, high-impact improvements and expanding from there.

How to read this article

For banking executives, department heads, and risk officers, we recommend skipping straight to part three (Why Bank AI Projects Fail at the Implementation Stage). It exposes the underlying friction points in most rollouts, giving you the necessary context to fully assess the hands-on execution steps we lay out at the end.

Why It Is Harder for Banks to Move Toward AI Orchestration

Over the years, legacy banking infrastructure has earned a reputation for resembling a bowl of spaghetti because institutions have implemented technology one isolated piece at a time (throughout successive digitalisation cycles in the last 20 years).

Instead of designing a unified system from scratch, banks brought in one tool to process loans, lease a totally different program to check IDs, and build a separate database to track fraud.

Now banks have multiple ways to interact with their customers, but they don’t have that connective intelligence layer required to to stitch those daily interactions into a smooth and unified customer journey.

This instability prevents banks from scaling intelligence effectively, and the roadblocks run across three distinct layers:

Layer 1: The technology stack

While a bank might look like a single, unified entity to a customer logging into a mobile app to make transactions, the infrastructure under the hood usually operates like a dozen completely independent companies.

According to Merkle’s 2025 "From Data Silos to Customer Insights" analysis, the average established bank still runs on 10 to 15 separate core systems that do not naturally communicate with each other, which makes them isolated data islands.

In simple terms, bank teams are forced to rely on a web of complex middleware and manual workarounds just to get through their daily tasks.

Layer 2: The data problem

While historical industry estimates note that roughly 80 percent of an enterprise's internal data is unstructured or locked in silos, recent data shows how fatal this is for modern initiatives.

Gartner predicts that through 2026, organisations will abandon 60 percent of their AI projects specifically because they are unsupported by AI-ready data. In banking, data is fiercely hoarded, trapped in vendor-specific formats, and hidden behind departmental firewalls.

Instead of having the comprehensive context needed to make accurate decisions, the AI is starved for information.

Layer 3: The organisational layer

The historical failure rate for digital transformation has always hovered around 70 percent, but the shift to artificial intelligence is proving even more difficult.

Recent findings from McKinsey and BCG reveal that over 80 percent of enterprise AI implementations fail to generate meaningful financial returns, and organisational silos are a primary cause.

Banks are still institutions that are built as separated divisions and are organised vertically by product—mortgages, wealth management, retail checking, etc.

AI, however, needs to analyse the customer's entire profile across every division in the bank, so connecting data across departments could slow implementation, especially since customer data is sensitive.

How JPMorgan Chase Overcame Legacy Silos to Scale AI

It’s easy to look at the fragmented state of banking tech and assume enterprise-wide AI is an impossible goal.

But it’s not and JPMorgan Chase is the textbook example of doing it right.

They achieved this by executing a massive, multi-year technology overhaul.

Long before generative AI became mainstream, leadership directed a $17 billion annual technology budget toward dismantling their old infrastructure.

They modernized their foundation through three specific steps:

Massive Cloud Migration: They migrated 80% of their business applications out of old, isolated data centers and moved 90% of their analytical data into highly automated public cloud environments.

Centralizing Data Infrastructure: Instead of leaving customer and financial data trapped inside separate departmental silos, they pooled their data into unified cloud environments. This allowed systems from completely different divisions to safely communicate with one another.

Deploying Proprietary Enterprise Tools: With a clean data foundation established, they built secure, in-house AI platforms. A 2025 Harvard Business School case study titled JPMorganChase: Leadership in the Age of GenAI details how this infrastructure allowed the bank to scale its "LLM Suite" to 200,000 employees, alongside specialized applications like "ChatCFO" to automate complex workflows.

As a result, a unified network generates between $1 billion and $1.5 billion in annual business value by driving instant fraud detection and faster operational workflows.

So if there are successful examples within the industry, why are so many other AI banking initiatives stalling?

Why Bank AI Projects Fail at the Implementation Stage

It is easy to point the finger at the technology or tight budgets when an AI initiative grinds to a halt, but the actual root of the problem almost always traces back to the organisation itself, usually showing up as poor management decisions and a total lack of clear ownership.

Daragh Morrissey, who leads financial services AI at Microsoft, sees the same thing across the banks he works with.

He pointed out that the technology is maturing quickly and that the barriers which remain are organisational rather than technical, rooted in data, process, and skills rather than in the models themselves.

According to him, and to Microsoft's 2026 Work Trend Index, the banks that manage to get AI projects into production set themselves apart because their CEO acts as a Chief AI Officer who pulls the business and IT to the same table.

Results show that organisational factors, things like culture, manager support, and talent practices, account for more than twice the impact on AI outcomes that individual skill and mindset do, 67 percent against 32.

A bank can hire capable people and watch the work go nowhere, because the institution around them was never rebuilt to use what they can do.

So how does it translate to making the decisions that lead to the problems that make AI implementation stall?

From our experience, it usually comes down to the same five, and they show up earlier than anyone expects.

Buying the tool before the main problem is understood

Leadership teams routinely fall in love with a flashy demo and sign the contract before figuring out what they actually need the platform to do.

Suddenly the bank owns a tool, and the immediate focus shifts to finding a way to justify it, which usually ends up with the team wasting months trying to twist their real-world problems to match the rigid new platform.

Instead of choosing the tool first, the organisation must isolate one strong case that needs immediate attention and calculate the exact hours and revenue lost to that bottleneck before evaluating vendors or looking to implement a custom AI solution.

Testing the model on data the bank will never actually run

When an automated underwriting model is piloted, it usually gets tested in completely artificial conditions.

The historical records provided for the trial are perfectly formatted for this purpose, with past errors already reconciled and anomalies manually corrected long ago.

So, for example, if the tested model is handed over to the loan department, it usually breaks down because daily operations involve a much messier reality of half-legible scans, mismatched dates across different forms, and incomplete customer uploads.

Proving a system works exclusively on perfectly clean files means preparing for a world the bank does not inhabit. Leadership usually discovers the technology fails exactly when the rollout begins and the pressure is highest.

Designing the tool without the people who do the job

If you leave key people out of the initial building phase, the AI will rely entirely on the available data or the rulebook, and will completely miss the human instincts employees depend on to do the job safely.

For example, a seasoned loan department officer will know to look past a perfectly typed business plan when the actual bank statements show erratic cash flow.

Failing to ask these employees for their input will guarantee that their real-world experience never makes it into the final solution.

This is just one example, but it points to a larger issue. Deploy a flawed solution, and the team will abandon the new setup within days and slip back into their old ways of working.

Leaving compliance until the model is nearly built

Even if the AI model passes every technical test with flying colours only a single regulatory question at the final review could send months of work back to the starting line.

It’s important to remember that laws will always require financial institutions to give a declined applicant a specific, defensible reason for the decision, rather than an automated output that nobody understands.

Bringing a risk officer into the very first planning meeting will weave this legal requirement into the system from day one, which costs almost nothing to do.

Leaving him/her out until the project is nearly finished will force that same officer to become the person who stops the launch, right after the bank has already spent the money to build it.

A Playbook to Scale AI in Banking Without Disrupting Legacy Operations

As we mentioned earlier, AI implementation is a process where leadership has to be at the forefront to lead the strategy.

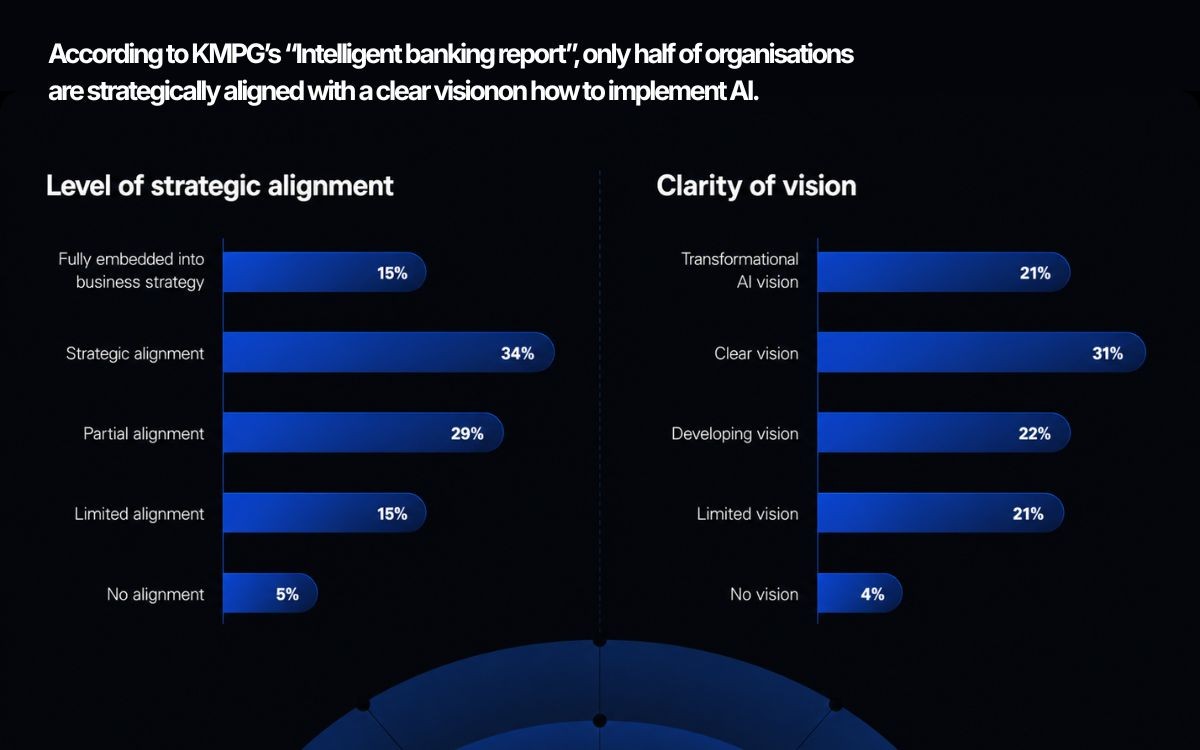

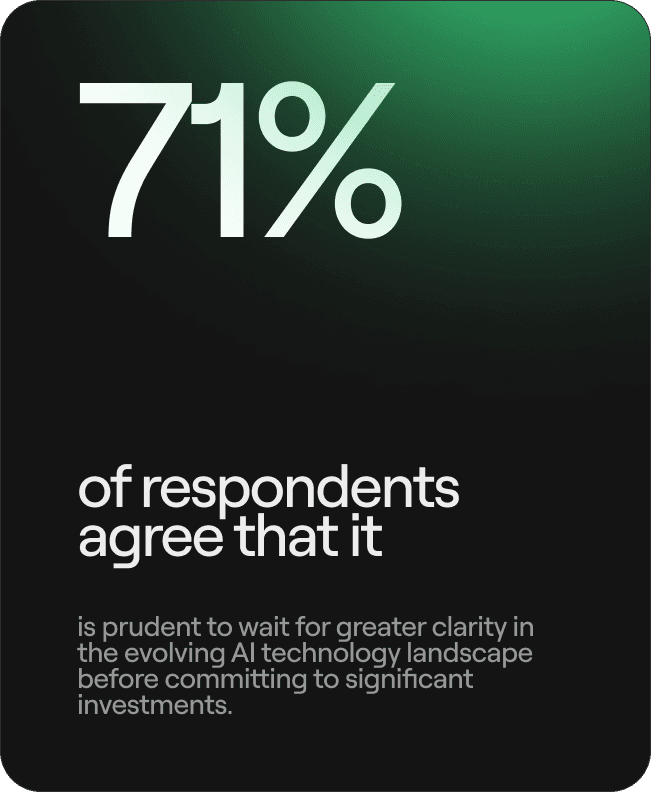

Executives need to figure out exactly what short-term gains they want to secure today, while actively preparing for their long-term objectives. It makes complete sense when you look at the numbers.

While 80 percent of banking executives believe AI will give them a competitive edge , 70 percent are facing intense shareholder pressure to show immediate returns.

Once leadership locks in a clear vision, it becomes much easier to build a structure that allows for better resource management, builds real internal capabilities, and aligns every AI initiative across the board.

So, where do you actually start?

How to Structure Your AI Rollout in Three Main Phases

To get AI running across a bank without overwhelming the systems everyone currently relies on, the deployment needs to happen in specific stages.

It is about balancing the push for new technology with the reality of keeping the daily work moving.

Phase 1: Enablement

Getting the groundwork right means tossing out the boring training manuals.

To actually get staff on board, teams need to get their hands dirty with the technology. This phase focuses on picking specific, high-value use cases and letting employees run small test projects across different departments.

By figuring things out in a controlled setting, the staff naturally picks up new skills and finds creative ways to solve daily problems.

For the bank, this hands-on approach delivers quick victories that prove the concept works. It allows the business to see immediate value without trying to overhaul the massive, rigid core systems all at once.

Phase 2: Integration

When those early test projects prove they can deliver real results, it is time to take off the training wheels.

This stage is about “connecting” the technology directly into the actual daily workflow. Instead of using a smart tool to speed up one isolated task, the goal shifts to upgrading complete, start-to-finish operations.

Think about the entire lifecycle of approving a mortgage or bringing a brand new client on board.

Upgrading these massive processes requires a total redesign of how work gets done across the board.

It forces departments that traditionally ignore each other to break down their walls and share information.

Phase 3: Evolution

Passing the integration test unlocks the ability to look outward and adapt to larger market disruptions.

In simple terms, if all that internal information is properly connected, the bank can use the technology to start predicting what people need instead of just reacting when someone asks for help.

If the system notices a sudden change in a customer's spending, it can offer a helpful fix before the client even has to pick up the phone.

This is also the stage where the bank starts teaming up directly with other companies. If they connect their services with outside financial planners or health apps, they create one smooth experience for the user.

4 Steps for a Smooth Operational Rollout

Moving a massive organisation through these three stages without breaking your daily operations takes a very specific approach on the ground.

The banks that successfully pull this off rely on four practical habits to ensure the technology actually transforms the business, rather than just disrupting it.

1. Target actual bottlenecks

Instead of rushing to adopt the latest AI trend just to look innovative, banks need to focus on concrete problems.

If a bank struggles to spot fraudulent transactions before they happen, or if it takes three weeks to approve a standard business loan, the new technology needs to solve those exact issues.

If a system does not directly speed up a slow process or protect the bank's money, it is a waste of resources.

To put this into practice:

Pinpoint the exact delay: Ask the department heads exactly which manual process costs the bank the most time or money.

Set a baseline: Document exactly how long that process takes right now, so you have a hard number to measure success against.

Run a closed test: Apply the new technology to historical data to see if it actually fixes the bottleneck without breaking anything else.

Launch with a single team: Let a small group of employees use the tool on live problems and fix the bugs before pushing it out to the rest of the floor.

2. Prove exactly how decisions are made

Handing high-stakes financial decisions over to an AI-driven system requires strict oversight.

If a system suddenly freezes a company's accounts because it suspects money laundering, the bank cannot just tell the client and the government that AI agent made the call.

They have to build strict rules for transparency right from the start.

The staff must be able to look under the hood and trace exactly which data points triggered the alarm so they can justify the action to regulators and avoid crippling legal fines.

To put this into practice:

Involve legal early: Bring the compliance team in to review the software's boundaries before writing any code.

Map the inputs: Document exactly what customer information the system is allowed to use to make a calculation.

Build the audit trail: Ensure the software is programmed to generate a plain-text log explaining exactly why it made a specific choice.

Test the explanation: Have non-technical employees read the log to ensure they can confidently explain the decision to a frustrated customer.

4. Elevate the staff's daily work

If employees think a new system is being brought in to phase them out, they will actively resist using it.

Leadership has to prove how the technology upgrades their roles.

When the staff sees the system handling the massive data extraction so they can spend their time actually negotiating deals and advising clients, the internal pushback completely vanishes.

To put this into practice:

Identify the worst tasks: Ask the floor workers which repetitive, manual chores drain the most hours from their week.

Clarify the goal: Communicate explicitly that the technology is being installed to handle those exact chores, not to replace the workers.

Provide hands-on training: Give the staff time to safely practice using the new tools on dummy contracts or fake client files.

Shift the daily focus: Officially redirect the hours they just saved toward high-value work, like direct client strategy and relationship building.

Frequently Asked Questions

Still have questions? We’ll guide you through with the answers.

We have an idea for an AI tool, but we do not want to commit a massive budget until we know it actually works. How can we safely test the concept?

We remove that financial risk by running an AI discovery workshop. Instead of spending weeks writing theoretical plans and reviewing static design files, we build a functional prototype.

You provide your core business rules and a sample of sanitized data. We map the architecture and deliver a working, clickable model within a single week.

Your stakeholders can interact with the live environment immediately to expose any hidden technical flaws and validate the user experience. This gives you a proven blueprint and complete certainty that the system functions correctly before you allocate the main engineering budget.

We run our core operations on older legacy systems. Do we have to replace our architecture to integrate your AI tools? No.

Replacing foundational systems carries an unacceptable level of operational risk and downtime.

Instead, we build secure API gateways and data pipelines that act as a bridge. We extract the necessary data from your older servers, clean it, and feed it into the new tools. Your core systems continue operating exactly as they are, and the AI software functions securely alongside them.

How do we determine which banking process to automate first?

We look directly at your operational costs and processing times. We sit down with your department heads to find the highest-volume manual tasks, like cross-checking compliance documents or extracting liability clauses from commercial loan contracts. If a proposed AI tool does not have a strict, measurable business case attached to it, such as reducing a three-day manual review process to two hours, we advise against building it.

What is the actual timeline to deploy these tools without disrupting our daily operations?

We roll out the technology in strictly controlled, isolated phases. Within the first few weeks, we test the system using offline, historical data to prove it accurately solves the problem.

Once verified, we deploy it to a single, specific team to catch any practical, day-to-day issues. This means you have a functioning tool operating safely in a controlled environment well before we scale it across the wider organization.

How do we manage staff who fear this software is being installed to replace them?

We position the rollout entirely around task reduction. We explicitly show your employees that the software is built to handle the massive data extraction and manual cross-referencing they already dislike doing.

Once the staff sees that the system handles the heavy data processing so they can spend their hours directly advising clients and negotiating deals, the internal resistance drops.